FX management reporting: what metrics does the board need?

FX mismanagement has ended careers. Tom Alexander outlines the six metrics every board needs to see, and why most CFOs struggle to produce them cleanly.

Understand how the forward curve and market risk views enable more strategic FX decisions before you trade.

When deciding whether and how to hedge FX exposure, most finance teams are trying to answer a single question:

Is the cost of hedging now greater than the currency risk we are trying to protect?

TruHedge is designed to answer that question instantly, before a trade is executed, using two complementary views. It compares the cost of forward-rate hedging with market-expected risk, so you only hedge when it genuinely adds value.

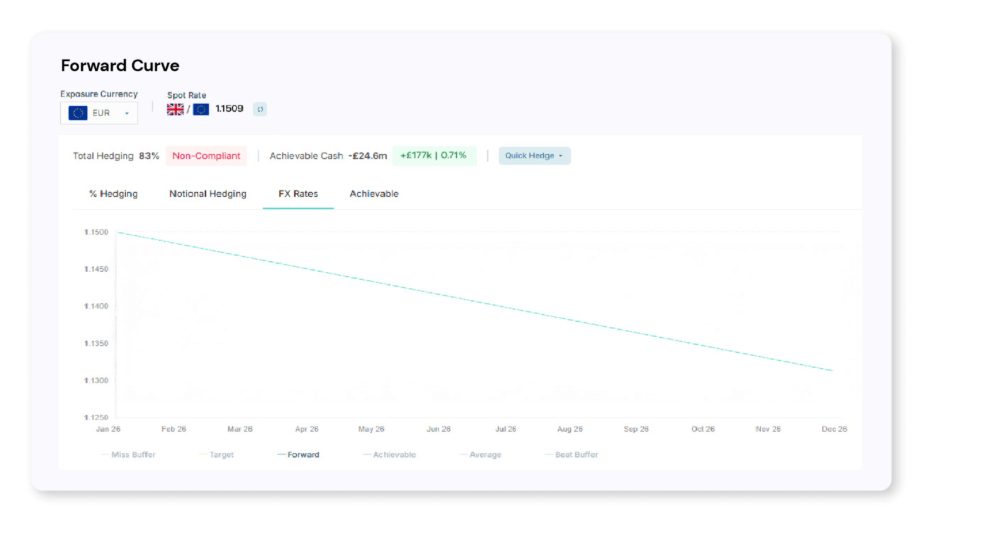

This view shows the forward curve for the selected currency pair, illustrating how the forward price evolves over time

The forward points curve reflects the cost or benefit of fixing an exchange rate today for settlement in the future. These movements are driven by interest rate differentials between the two currencies.

Where a company is buying a currency with a lower interest rate than the sell currency, the forward rate deteriorates over time, creating a cost to hedge relative to spot. While some businesses accept this as a cost of doing business, others may become less competitive or less profitable if they hedge fully while peers do not.

In the example shown:

This view makes the cost of hedging over time visible before any trade is executed, based on the forward curve, before counterparty pricing is applied.

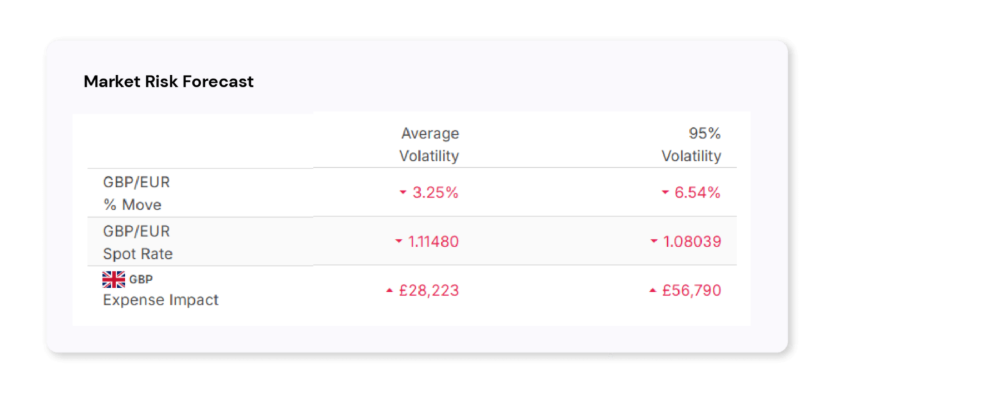

The second view shows the potential downside based on historical data over the same time period.

This view translates FX market uncertainty into measurable terms by showing implied volatility across the horizon, both on an average and high-confidence basis.

In the example shown:

(These are taken from the last 4 years volatility data over this time period, for this currency pair)

This answers a different but equally important pre-trade question:

How much could the market realistically move over this period?

Rather than treating FX risk as an abstract concept, TruHedge quantifies it in a way that can be directly compared to forward cost.

When the forward curve and market-expected risk are considered together, TruHedge enables a decision that most finance teams are unable to make pre-trade: whether hedging now adds value, or whether waiting and layering risk is the smarter choice.

On one side is the known forward cost of hedging today, shown by the forward curve. On the other is the uncertain market risk of leaving exposure open, expressed through estimated volatility.

In this example, the forward cost to December is approximately 1.51 %. Over the same period, average estimated volatility suggests the market could move by around 3.25 %, but that risk may or may not materialise.

Fully hedging the exposure today would therefore lock in a known cost in exchange for removing an uncertain, probabilistic risk.

The difference between these two represents an opportunity cost of approximately 1.73 %, which on a €20 million hedge equates to just under €350,000 in cash terms, a trade-off that becomes visible before any hedge is executed.

Smarter hedging starts with better information

Armed with this information, finance teams are no longer limited to a simple yes-or-no hedge decision. Instead, TruHedge supports more nuanced approaches, such as layered or descending wedge hedging strategies.

By hedging more on nearer settlement dates and less further out, then topping up exposures over time, businesses can:

This approach balances certainty and flexibility, without stepping outside a disciplined risk framework.

If you would like to speak with one of our partners about your FX needs and how TruHedge is transforming FX management, please get in touch at connect@tenora.com.

Take the first step towards smarter, more transparent FX decisions.

Our blog